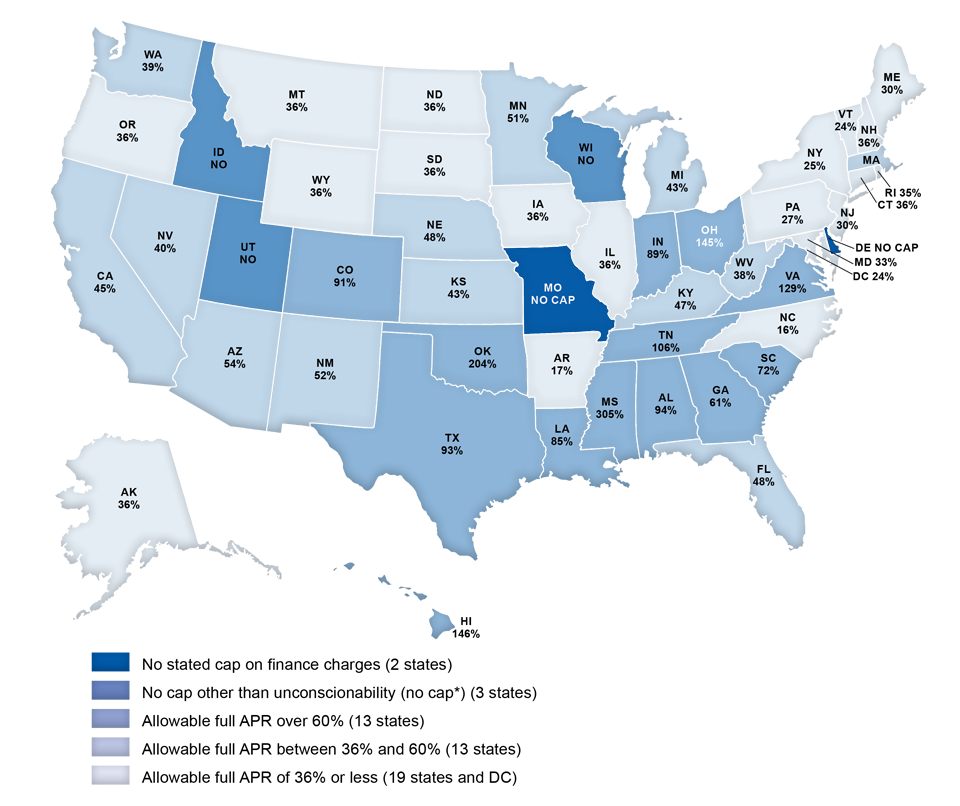

In the past few years, a wave of predatory lending has surged under the banner of rent‑a‑bank schemes. These arrangements allow high‑cost lenders to slip their loans through FDIC‑supervised banks that are not bound by state usury laws, effectively bypassing caps that would otherwise protect consumers.

The practice is more than a legal loophole; it’s a financial minefield for anyone looking for quick cash. As the number of states tightening enforcement grows, lenders are scrambling to find new avenues—often at the expense of borrowers who end up with sky‑high interest rates and hidden fees.

How Rent‑a‑Bank Schemes Work

The core idea is simple yet sinister: a non‑bank lender partners with a bank that has no state license, or one that is exempt from local usury limits. The lender supplies the loan terms—principal, APR, repayment schedule—while the bank issues the actual money to the borrower.

Because the bank’s charter does not carry the same regulatory baggage as a traditional state‑licensed lender, it can provide funds at rates far beyond what would normally be permissible in that jurisdiction. The borrower, however, is unaware of this behind‑the‑scenes arrangement and believes they are dealing with a standard financial institution.

In many cases, the bank is a small, FDIC‑supervised industrial or community bank—often headquartered in Utah or Kentucky—while the lender operates under an umbrella brand that markets itself as a “consumer finance” provider. This dual identity makes it difficult for regulators to pin down responsibility.

Typical Loan Products

- Installment Loans: $500–$10,000 with APRs ranging from 140% up to a staggering 225%. These are marketed as “quick cash” or “personal loan” options for consumers with limited credit.

- Auto‑Title Loans: Short‑term loans secured by a vehicle’s title, often advertised through auto dealerships or online portals. Rates can reach 170% APR on three‑year terms.

- Retail Installment Financing: Credit extended for purchases of furniture, appliances, or electronics, with hidden insurance and service fees added to the cost.

Key Players in the Ecosystem

| Lender | Bank Partner | Typical APR Range |

|---|---|---|

| Personify Financial (Applied Data Finance) | First Electronic Bank (Utah) | 140%–180% |

| Elevate Capital | Republic Bank & Trust (Kentucky) | 95%–110% |

| CNG Holdings (Check ’n Go) | Capital Community Bank (Utah) | 145%–225% |

| EasyPay Finance | Transportation Alliance Bank / TAB Bank (Kentucky/UT) | 150%–190% |

| LoanMart (Wheels Financial Group) | Community Capital Bank (Utah) | 160%–170% |

The table above highlights how the same bank can be a conduit for multiple lenders, each offering rates that would be illegal in most states. It also underscores why regulators are focusing on these partnerships rather than individual lenders alone.

State‑Level Enforcement and Legal Actions

Over the past year, more than a dozen state attorneys general have joined forces to file lawsuits against major players in the rent‑a‑bank arena. The suits allege that these lenders are engaging in deceptive practices by hiding costs, misrepresenting product terms, and exploiting borrowers who lack alternatives.

The most high‑profile case involves OneMain Financial, which was sued by 13 attorneys general over hidden loan add‑ons such as credit insurance. While not a classic rent‑a‑bank operation, the lawsuit illustrates the broader trend of regulators cracking down on any lender that leverages opaque arrangements to inflate costs.

In parallel, federal agencies—including the Consumer Financial Protection Bureau (CFPB) and the Department of Justice—have launched investigations into the structure of these schemes. Early findings suggest that many lenders rely on “layered” financing models that make it difficult for borrowers to trace the true source of their debt.

Recent Legal Developments

- 2026‑03‑16: OneMain Financial faces a lawsuit over hidden add‑ons, setting a precedent for scrutinizing bundled fees in consumer loans.

- 2026‑02‑26: The National Consumer Law Center (NCLC) publishes an issue brief on high‑cost rent‑a‑bank lenders, calling for tighter oversight of FDIC‑supervised banks used as conduits.

- 2026‑01‑10: Several states amend their usury statutes to explicitly include loans issued through bank partnerships, closing a loophole that had been exploited by non‑bank lenders.

These legal actions have forced some lenders to halt operations in certain jurisdictions. However, the sheer number of state laws and the variety of bank structures mean enforcement remains uneven across the country.

What Borrowers Should Watch For

If you’re considering a quick loan, especially one that promises low monthly payments or flexible terms, read the fine print closely. Look for red flags such as:

- Excessive APRs: Rates above 100% are usually illegal in most states.

- Hidden Fees: Insurance, service charges, or “processing” fees that aren’t disclosed upfront.

- No State License: If the lender’s website claims it is licensed in your state but you cannot verify it through the state banking department, proceed with caution.

- Rapid Approval Promises: Quick decisions are common among predatory lenders; legitimate banks often require a thorough credit check.

In many cases, borrowers can protect themselves by seeking alternatives such as credit unions, community banks, or online lenders that have transparent terms and are fully licensed in their state. Additionally, tools like FastLendGo Personal Loan Solutions Hub provide a quick way to compare rates from reputable lenders who comply with local regulations.

Using Credit Counseling Services

If you find yourself trapped in a high‑cost loan, credit counseling agencies can help negotiate lower rates or restructure debt. The CFPB recommends certified counselors who are licensed and have a track record of successful negotiations. While counseling does not erase the debt, it often reduces monthly obligations enough to prevent default.

Reporting Illegal Activity

Borrowers who suspect they’ve been defrauded can file complaints with:

- The Consumer Financial Protection Bureau (CFPB).

- Your state’s Attorney General office or Department of Banking.

- FDIC, if the lender is a bank or uses a bank as a conduit.

Document all communications and keep copies of loan agreements. These records are crucial for investigations and potential legal action.

The Road Ahead: Regulatory Trends

Regulators appear committed to closing the gaps that allow rent‑a‑bank schemes to thrive. Anticipated developments include:

- Expanded Usury Laws: More states are likely to amend statutes to explicitly cover loans routed through partner banks.

- Stricter Licensing Requirements: Banks used as conduits may face new compliance checks and reporting obligations.

- Consumer Protection Campaigns: Public awareness initiatives will aim to educate borrowers about predatory lending tactics.

Meanwhile, the fintech landscape continues to evolve. Some legitimate lenders are adopting “open banking” APIs that allow for faster underwriting while still adhering to state caps. Others are partnering with credit unions or community banks to provide competitive rates without resorting to opaque structures.

Industry Response

In response to mounting scrutiny, several large non‑bank lenders have announced plans to streamline their operations and focus on compliance. One major lender has pledged to halt all activities that involve banks exempt from state usury limits by the end of 2027.

For consumers, the best defense is vigilance: compare rates, verify licensing, and use reputable platforms—such as FastLendGo Personal Loan Solutions Hub—to find loans that respect state regulations.

Key Takeaways for Borrowers

- High‑cost rent‑a‑bank lenders often hide behind bank partnerships to offer illegal APRs.

- State and federal regulators are tightening enforcement, but gaps remain.

- Borrowers should verify licensing, read fine print, and consider reputable alternatives.

- Tools like FastLendGo can help compare compliant loan offers quickly.

By staying informed and cautious, borrowers can avoid falling prey to predatory lending practices that have long plagued the financial landscape. As regulation tightens, the hope is for a safer borrowing environment where transparency and fairness are no longer optional but standard practice.